FIG. 1. Thought diagram showing that future projections of consumer chemicals demand are stronger than projections of fuels demand.

The refining industry links the upstream production of crude oil with the end markets for fuel products, as well as for the petrochemical/chemical industry. Refineries have been investing in complex facilities to improve conversion and to better alter the final product composition..

and quality to adhere to changing market and regulatory requirements. For example, by using a combination of or stand-alone fluidized catalytic cracking unit (FCCU) and hydrocracking capacities, refineries can orient output to adhere to a wide range of gasoline/diesel ratios. Similarly, a bottoms upgradation facility enables refiners to eliminate or minimize fuel oil per market demands. However, a mismatch in refinery output and local market demand can still exist. This predicament drives the need to either export fuels or divert product volumes to petrochemicals/chemicals. Drivers for higher petrochemical feedstocks were traditionally regional and driven by a combination of the local fuel demand mix (e.g., diesel/gasoline ratio and LPG demand/composition), competitiveness in fuel export markets and the availability of natural gas as feedstock for steam crackers.Petrochemicals are projected to be the largest driver of world oil demand growth, surpassing that of gasoline or diesel by 2030. Drivers for this change are the growing electrification of vehicles and the increasing fuel efficiency of new vehicles. Therefore, integrating petrochemical production capacity into refineries is imperative to solve the mismatch in local market supply and demand. In this scenario, non-integrated refiners and petrochemical producers with less flexibility will be more vulnerable to demand risks. Refiners and chemical producers will respond by developing integration synergies uniquely tuned for each site. However, there is no one-size-fits-all option. The best option will be chosen by examining product opportunities, facility configurations, technologies, logistics and return on capital.

The most common and practicable ways that refineries are integrated with petrochemical production include:

. A refinery integrated with a steam cracker

. A refinery integrated with an aromatics complex

. A refinery integrated with a steam cracker and aromatics complex

. Downstream chemicals integration with the above routes.

In conventional refinery integration, excess naphtha and LPG were allocated to the cracker and aromatics complex. In the revised scenario of plateauing fuels demand, refiners have started selecting technologies with the intent to divert more distillates toward steam crackers and aromatics. Alternately, some refineries elect to focus on fuels and to divert excess naphtha/LPG to a separate petrochemical facility rather than having an integrated complex. These are two extremes of a continuum of possible refinery configurations.

Synergies: Stand-alone vs. integrated refinery/petrochemical complexes

In the non-integrated scenario, refineries have been selling naphtha to other independent steam cracker and aromatic complexes. However, there are significant premiums in integrating these complexes at a single site, which allows consolidation of the intermediates and monetization of the synergies. The advantages are multifold:

. Olefins command significant premium over transportation fuels

. The impact of demand and price fluctuations on profitability are dampened

. More options exist to alter product slates to respond to market needs

. Ensured feedstocks availability for petrochemicals

. Value enhancement from integrating intermediate streams

. Capital and operating costs and resource optimization, savings from which can be further attributed to the following:

Shared infrastructure and utilities

Lower transportation costs

Minimization of fixed overheads.

Some of the strategies that can be critical in the economics of integration are discussed in the appending section. These include:

. Hydrogen sharing between the refinery, cracker and aromatics increases flexibility

. Combining ethylene/propylene recovery from the FCCU/coker offgas with the cracker

.Multiple options in optimizing the C4 stream, including producing butadiene/butenes, hydrogenation and recycle to the cracker, or adding to LPG

. Upgrading pyrolysis gasoline to avoid the production of negative value products (i.e., those with value lower than the cracker feed). Some options include:

C5 diolefins can be utilized to manufacture dicyclopentadiene, depending on market requirements. Alternately, C5s can be hydrogenated and recycled to the cracker or added to the gasoline pool.

Pyrolysis gasoline contains over 60 wt% C6–C10 aromatics, half of which is benzene. The C6 cut can be fed to extractive distillation for producing benzene.

The C7+ cut has an excellent octane rating and can be advantageously sent to the gasoline pool. When demand for benzene is high, the C7+ cut can be sent to the hydrodealkylation process to be converted to benzene.

The C7–C8 streams can also be integrated with the aromatics section for paraxylene (PX) yield enhancement.

The C9+ cut can be absorbed in the diesel pool.

. Raffinate from the aromatics complex is blended in the gasoline pool.

. Heavy aromatics from the aromatics complex is blended in the diesel pool.

FIG. 2. illustrates the common synergies between the refinery, petrochemical and aromatics complexes.

FIG. 2. Synergies among refinery, petrochemical and aromatics complexes.

A high-level integration case study has been developed to illustrate the possible alternate grassroot configurations and their directional impact on refinery margins and rates of return. The location of the complex is a key driver in overall project economics, since relative fuels/chemicals pricing, fuel costs, crude/product freight impact and capital expenditures (CAPEX) are all dependent on where the project is located. For the purpose of this study, the location of the new complex is in India.

Fuels and petrochemicals outlook for India

India is emerging as one of the fastest growing economies in the world. With a total capacity of 250 MMtpy, India is the fourth largest refiner in the world. It is positioned to serve domestic demand of petroleum products and to supply petroleum products to other Asian countries.

A high population and relatively low per capita consumption show the promise of high economic growth rates for the energy sector and consumables. In addition to fuels, chemicals and petrochemicals also have vital stakes in economic growth—namely agriculture, infrastructure, health care, textiles and consumer durables. Petrochemical products cover the entire range of consumables and durables, ranging from clothing, housing, construction, furniture, automobiles, household items, toys, agriculture, horticulture, irrigation and packaging to medical supplies. Between 2015 and 2040, India’s GDP growth rate is forecast to be more than 7%.

Some relevant projections for the Indian refining and petrochemicals sector are:

. Petroleum product demand is forecast to increase to 472 MMtpy by 2040.

. Diesel and gasoline consumption are forecast to increase at a compound annual growth rate (CAGR) of more than 4% to 2040.

. Domestic refining capacity is projected to increase by 224 MMtpy by 2040.

. More than 5 MMtpy of polypropylene (PP) capacity is expected to be added by 2025.

. More than 4 MMtpy of high-density polyethylene (HDPE) and low-linear-density polyethylene (LLDPE) capacity is forecast to be added by 2025.

. By 2025, India is forecast to have a deficit of purified terephthalic acid and PX of 1.8 MMtpy and 600,000 tpy, respectively.

Additional parameters relevant to the Indian fuels and chemicals scenario that have a significant bearing in setting the boundaries of the integration case study are as follows:

. Fuel demand is skewed toward diesel (3:1 diesel-to-gasoline ratio).

. Naphtha is the primary feedstock for steam crackers, since cheap domestic natural gas is scarce.

. LPG specifications can absorb up to 80% C4s.

. Research octane number (RON) and motor octane number (MON) specifications for regular grade Bharat Stage 6 (BS-6) gasoline (91 and 81) are lower than Euro 6 gasoline (95 and 85).

. Olefin content is limited to 21% in the BS-6 specification for regular grade gasoline. This is slightly greater than the maximum of 18% specified for Euro 6 gasoline.

. Capital costs in India are significantly lower vs. in the U.S. Gulf Coast and the Middle East.

. A significant domestic supply shortfall (more than 50% by volume) in several petrochemical intermediates exists, primarily from six major value chains in petrochemical intermediates.

. Utility costs are higher, as utilities are majorly captive, and centralized utility providers are rare.

Case study methodology

The case study illustrates the investment analysis for a hypothetical integrated refinery/petrochemical complex. The objective is to demonstrate the impact on refinery margins and returns as the product slate is shifted from fuels to petrochemicals. A simple model is constructed to reasonably capture the product slate of the alternate configurations based on typical yields from different technologies. This simplified model has constant yields in units (such as FCCUs) in high-severity mode with a fixed feed of hydrotreated vacuum gasoil (VGO), and does not vary, thus optimizing the feed, operating conditions or yields for each case. There are trade-offs in selecting this simplified approach in relation to the rigorous LP model. This model will not simulate all possible combinations of design variables and optimized solutions. Uncertainty exists in future demand projections, and directly coupling of such highly estimated data with sophisticated LP subroutines will not add value. Alternately, the results from this directional assessment can be utilized as guides in screening and for carrying out site-specific optimizations using the LP model. Feedstock and product prices are based on 3-yr averages, which should be adequate to capture average refinery margins (FIG. 3). The order-of-magnitude CAPEX for calculating the internal rate of return (IRR) is based on adjusting/scaling publicly available estimated project costs for similar projects/units in recent years.

FIG. 3. Price set—Added value on crude.

Base case

The base case (FIG. 4) refinery is configured for processing 15 MMtpy of light crude (API > 33), producing gasoline and diesel fuels. The base case refinery is equipped with a high-severity FCCU as the main VGO conversion unit, with an upstream VGO and heavy coker gasoil (HCGO) hydrotreater. The delayed coking unit (DCU) is selected for vacuum residue conversion. In line with demand patterns, the crude unit maximizes diesel production by dropping heavy-end kerosene material into the diesel cut. This configuration is capable of maximizing diesel, while still retaining the flexibility to add on petrochemical blocks by changing crude unit cut points and redirecting streams. Propylene is included as one of the intended major products from the base case refinery, which includes two 400,000-tpy PP units. The FCCU and DCU have world-scale capacities of more than 4 MMtpy.

FIG. 4. Base case: Fuels refinery.

Integration cases

The integration cases explore the common integration strategies and test the boundaries of the chemical conversion and economic margins that can be achieved. The following describes the integration case studies:

. Case 1: Refinery integrated with a steam cracker

. Case 2: Refinery integrated with an aromatics complex

. Case 3: Refinery integrated with a steam cracker and aromatics complex

. Case 4: Refinery integrated with a steam cracker and aromatics complex and downstream chemicals.

TABLE 1 provides a unit-level definition of these integration cases.

Case 1

Case 1 adds an aromatics complex to produce 1.2 MMtpy of PX from naphtha, as well as an ethylene recovery unit from FCCU/DCU offgases to produce mono-ethylene glycol (MEG) to the base case refinery. The units in the aromatics complex are high-severity reforming (continuous catalytic reformer), PX separation and purification, C8 raffinate isomerization, toluene and C9–C10 transalkylation, and benzene-toluene extractive distillation. The products produced from the aromatics complex are PX, benzene and hydrogen.

Case 2

Case 2 adds a 1.5-MMtpy mixed-feed cracker and downstream polymer units to the base case refinery. The key feedstocks considered for the cracker include:

. Offgases from the DCU (rich in ethane and olefins)

. Offgases from the FCCU (rich in ethylene and ethane, with some propane)

. LPG from the refinery pool

. Straight-run naphtha and kerosene streams to satisfy cracker capacity.

The proposed downstream configuration for Case 2 is:

. A world-scale swing unit to produce HDPE and LLDPE

. A standalone HDPE unit

. A 1-butene facility to satisfy the requirement in PE plants as a co-monomer

. Additional chains of PP units to convert propylene produced from the complex

. The generated C6 stream from pyrolysis gasoline hydrogenation will be charged into the benzene extraction unit from where C6 raffinate is recycled back to the cracker

. The hydrogenated C5 cut is recycled back to the cracker

. The C7+ stream is routed to the gasoline pool.

MEG production—diethylene glycol (DEG) and triethylene glycol (TEG) as byproducts—is not considered in this case, and all ethylene produced is consumed in the HDPE/LLDPE units.

Case 3

Case 3 combines Case 1 and Case 2 with the base case refinery (i.e., the aromatics complex and mixed-feed cracker in one single configuration). In addition to the standard downstream petrochemical units present in Case 2 (namely HDPE, LLDPE, PP and butadiene/1-butene), Case 3 also includes MEG production.

Case 4

This case is a modification of Case 3, adding downstream chemicals value chains for propylene and ethylene. These include cumene/phenol/isopropyl alcohol (IPA), propylene oxide (PO)/propylene glycol/polyol and styrene (as a co-product of PO). A significant demand and growth rate exist for these downstream specialty petrochemicals to support an investment in India. Case 4 is the highest extent of chemical integration that this case study explores. FIG. 5 represents a high-level block flow diagram to detail the major streams.

FIG. 5. Case 4 block flow diagram: Refinery, petrochemical and aromatics complexes, and downstream chemicals.

Considering local market requirements for a higher diesel-to-gasoline ratio, each configuration ensures that this ratio remains above 2, even as petrochemicals content is increased. In addition, LPG production is curtailed and diverted to the cracker in view of expected cheaper alternative sources. Diesel is the predominant fuel in India’s fuel mix, and, with a significant forecasted increase in the adoption of electric vehicles, future gasoline demand is less predictable. The configuration achieves world-class, single-train capacities for all major units/blocks, while limiting the refinery capacity to 15 MMtpy. This helps limit capital investment, while avoiding penalties due to economies of scale. This configuration allows the focus to be on satisfying local/national market requirements, as well.

Summary of results

The product slates, refinery margins, relative CAPEX and IRR for all cases are summarized in TABLE 2. This also provides an idea of the multitude of capacities that can be achieved for each product chain.

Sensitivity analysis

The global refining and petrochemical industries are forecast to undergo a massive shift due to forces emanating from either end markets or upstream feedstock prices. The choice of feedstock, demand patterns, government directives and return on capital requirements will influence configuration decisions. The following parameters of each case study have been varied to see the impact on each configuration:

. Lower diesel prices due to excess production

. Lower gasoline prices due to lower demand growth

. Lower prices for ethylene-based chemicals

. Lower prices for propylene-based chemicals

. Increase in CAPEX by 10%.

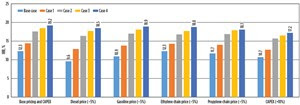

FIG. 6 details the IRR for each case for these sensitivity scenarios.

FIG. 6. IRRs for each case study for the sensitivity scenarios.

Summary of findings

Even this limited high-level study utilizing a simplified methodology leads to interesting conclusions. Increasing the share of petrochemicals in the product slate increases refinery margins and IRR. In this case study, while growth in refinery margins is almost linear, returns start to plateau as petrochemicals content approaches 30%. The sensitivity analysis demonstrates that an integrated refinery is better able to manage returns, even with a decrease in cracks and spreads. This makes the integrated complex more robust and resistant to swings in demand. For a higher percent of crude-to-chemicals conversion to be economically viable, margins need to be harvested from crude pricing, export-oriented product pricing, and elaborate residue upgrade investments for heavier crude processing, among others.

Several additional factors that need to be considered while specifying the configuration include:

1. A site-specific combination of factors (e.g., crude delivery infrastructure, location near demand markets, and land and construction costs) can boost or reduce refinery margins by $4/bbl–$8/bbl, which can significantly alter facility economics.

2. This case study considers a grassroots refinery focused on supplying the domestic market and exploiting local diesel demand. Integrating chemicals to an existing refinery or to a refinery focused on significant exports will be complex and will differ in several aspects.

3. Several options exist in configuring downstream chemicals. This case study selected a few of these options for illustration. For example, MEG is a capital-intensive process that is highly price sensitive. It has been considered in some cases, but not all. Another example is low-density polyethylene/ethylene vinyl acetate, a prospective niche petrochemical polymer, which is not considered here. This technology is licensed by very few licensors, as it has a high CAPEX and a significant proprietary content. Vinyl chloride monomer/polyvinyl chloride is also not considered, but can be added, provided an economical source for chlorine or ethylene dichloride can be found. Styrene and cumene/phenol/acetone have been included. This makes the benzene balance critical. A decision will need to be made on whether to import benzene or further convert the pygas C7+ stream. For this study, importing benzene was considered. The value chain can be extended to include polycarbonates and methyl methacrylates/poly methyl methacrylates. These can be taken up as site-specific enhancements.

4. The integration of petrochemical blocks increases CAPEX requirements and overall project complexity. This would require larger financial and execution resources. Construction time and ramp-up time until full production can be significantly higher for a large and complex integrated refinery, thus impacting return on investment (ROI).

5. The competitiveness of integrating petrochemicals with a refinery is dependent on two factors:

6. Relative competitiveness of naphtha vs. cheap, natural-gas-based feedstocks for the cracker. Considering a low oil price regime, it is assumed that naphtha-based crackers will remain competitive in India.

7. Integration is made more competitive by ensuring better integration with refinery streams and by achieving scale without diverting the diesel stream to the cracker or the aromatics complex. The investment costs are expected to be significantly higher in the latter option due to the additional units required to convert diesel to naphtha. Given the robust diesel requirement in the Indian market, this has not been considered in the current study.

8. The study is based on a single light crude; however, there does exist the option of utilizing heavier/cheaper crude slates. This will require changes to the refinery conversion configuration and alternate bottoms upgrading technologies, such as an ebullated-bed hydrocracker.

9. Several cutting-edge technologies are in the process of development and implementation. Thermal cracking of crude oil, along with improvements around the ethylene cracker to accept heavier feedstocks and higher-intensity hydrocracking, are some areas likely to attract significant research and development. When these newer technologies become commercially available, they have the potential to change the face of refining and petrochemical configurations.

10. Growth in consumer chemicals and plastics brings in environmental liabilities that are far too great to be taken lightly in the long term. Responsible growth strategies would require significant investments for the development of necessary infrastructures to support a sustainable culture of “protect, reuse and recycle.”

Refining is a capital-intensive industry operating between two related, but independent, markets for crude oil and finished petroleum products. Configurations and operations that deliver adequate ROI are a function of a complex set of variables. Some variables, such as competition with alternate feedstocks and declining growth in transportation fuels, are global in nature. These require devising more diverse product slates by including petrochemicals. Other variables (such as local market dynamics, feedstock/product logistics and construction costs) are site specific and are to be used to arrive at the correct mix of fuels and petrochemicals that will remain profitable in different market scenarios. The case study presented provides directional insights into the paradigm shift from fuels to chemicals. The data presented should be treated as conceptual views of the authors and not directly attributed to the authors’ organization. HP

Απο το hydrocarbonprocessing.com

Δεν υπάρχουν σχόλια:

Δημοσίευση σχολίου